Up to date on January 28, 2025, with up to date screenshots from H&R Block Deluxe obtain software program for the 2024 tax 12 months. For those who use TurboTax or FreeTaxUSA, see:

The earlier put up Break up-12 months Backdoor Roth in H&R Block, 1st 12 months handled contributing to a Conventional IRA for the earlier 12 months or recharacterizing a earlier 12 months’s Roth IRA contribution as a Conventional IRA contribution. This put up handles the conversion half.

We cowl two instance situations. Right here’s the primary state of affairs:

You contributed $6,500 to a Conventional IRA for 2023 in 2024. The worth elevated to $6,700 once you transformed it to Roth in 2024. You acquired a 1099-R type itemizing this $6,700 Roth conversion.

You need to’ve already reported the contribution half in your 2023 tax return by following Break up-12 months Backdoor Roth in H&R Block, 1st 12 months. The IRA custodian despatched you a 1099-R type for the conversion in 2024. This put up exhibits you easy methods to put it into H&R Block tax software program.

Right here’s the second instance state of affairs:

You contributed $6,500 to a Roth IRA for 2023 in 2023. You realized that your revenue was too excessive once you did your 2023 taxes in 2024. You recharacterized the Roth contribution for 2023 as a Conventional contribution earlier than April 15, 2024. The IRA custodian moved $6,600 out of your Roth IRA to your Conventional IRA as a result of your authentic $6,500 contribution had some earnings. The worth elevated once more to $6,700 once you transformed it to Roth in 2024. You acquired two 1099-R varieties, one for $6,600 and one other for $6,700.

You need to’ve already reported the recharacterized contribution in your 2023 tax return by following Break up-12 months Backdoor Roth in H&R Block, 1st 12 months. The IRA custodian despatched you two 1099-R varieties, one for the recharacterization, and the opposite for the conversion. This put up exhibits you easy methods to put each of them into H&R Block tax software program.

For those who contributed for 2024 in 2025 or in case you recharacterized a 2024 contribution in 2025, you’re nonetheless within the first 12 months of this journey. Please comply with Break up-12 months Backdoor Roth in H&R Block, 1st 12 months. For those who recharacterized your 2024 contribution in 2024 and transformed in 2024, please comply with Backdoor Roth in H&R Block: Recharacterized within the Similar 12 months.

If neither of those instance situations suits you, please seek the advice of our information for a standard “clear” backdoor Roth: Learn how to Report Backdoor Roth in H&R Block Tax Software program.

For those who’re married and each you and your partner did the identical factor, you must comply with the steps under as soon as for your self and as soon as once more to your partner.

Use H&R Block Obtain Software program

The screenshots under are taken from H&R Block Deluxe downloaded software program. The downloaded software program is extra highly effective and cheaper than on-line software program. For those who haven’t paid to your H&R Block On-line submitting but, think about shopping for H&R Block obtain software program from Amazon, Walmart, Newegg, and plenty of different locations. For those who’re already too far in getting into your knowledge into H&R Block On-line, make this your final 12 months of utilizing H&R Block On-line. Swap over to H&R Block obtain software program subsequent 12 months.

1099-R for Recharacterization

This part solely applies to the second instance state of affairs. For those who didn’t recharacterize (the primary instance state of affairs), please skip this part and soar over to the conversion part.

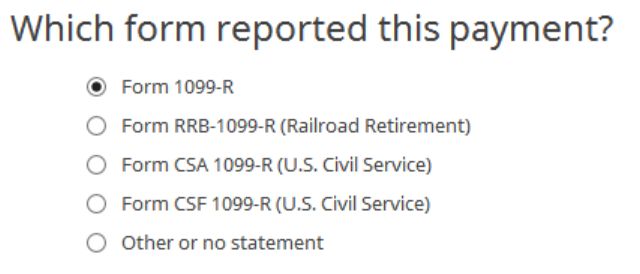

We deal with the 1099-R type for recharacterization first. This 1099-R type has a code ‘R’ in Field 7.

Click on on Federal -> Earnings. Scroll down and discover IRA and Pension Earnings (Kind 1099-R). Click on on “Go To.”

Click on on Import 1099-R in case you’d like. I present guide entries with “Enter Manually” right here.

Only a common 1099-R.

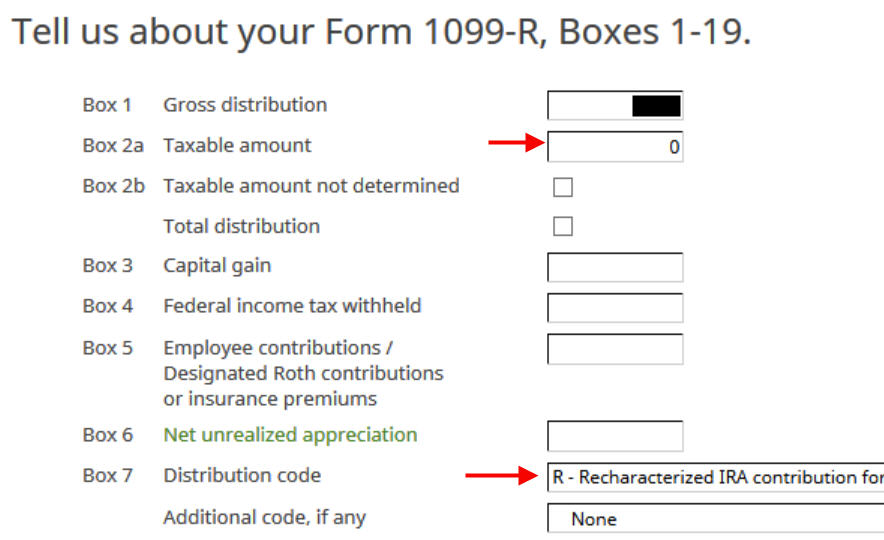

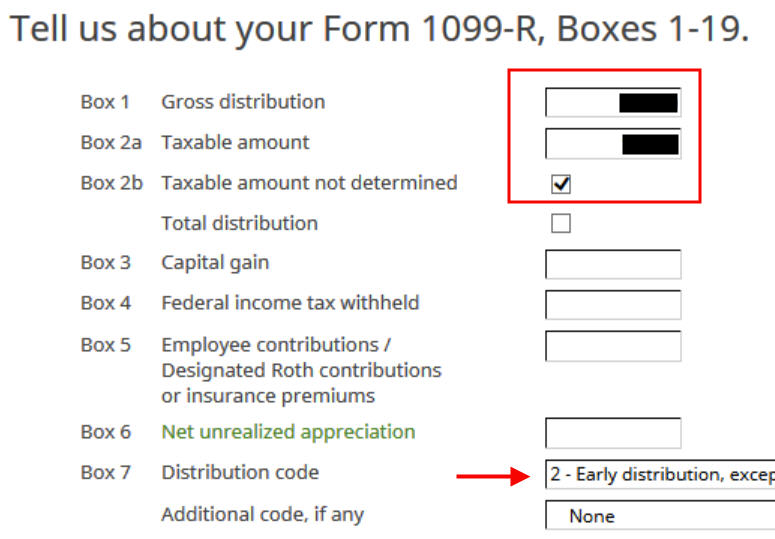

The quantity that moved out of your Roth IRA to your Conventional IRA is proven in Field 1. It’s $6,600 in our instance. The taxable quantity in Field 2a is zero. The 2 checkboxes in Field 2b aren’t checked. The code in Field 7 is “R.”

The “IRA/SEP/SIMPLE” field underneath Field 7 could or might not be checked. It’s not checked in our pattern 1099-R.

Not a retired public security officer.

We like to listen to that.

You’re executed with the primary 1099-R type. Click on on “Enter Manually” so as to add the second in case you don’t have already got each 1099-R varieties imported.

1099-R for Conversion

The 1099-R for conversion has both a code “2” or code “7” in Field 7.

The second 1099-R type can also be an everyday 1099-R.

It’s regular to see the conversion reported in Field 2a because the taxable quantity when Field 2b is checked to say “Taxable quantity not decided.” The code in Field 7 is ‘2‘ once you’re underneath 59-1/2 or ‘7‘ once you’re over 59-1/2.

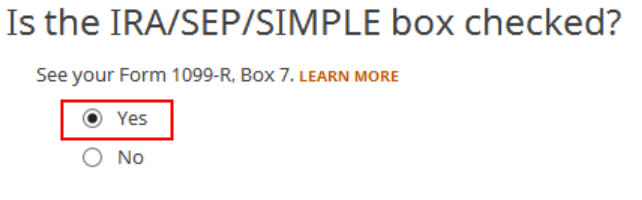

The “IRA/SEP/SIMPLE” field is checked on this 1099-R type for the conversion.

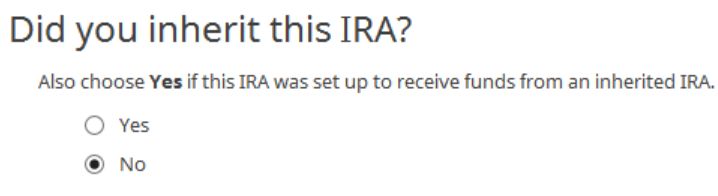

Didn’t inherit it.

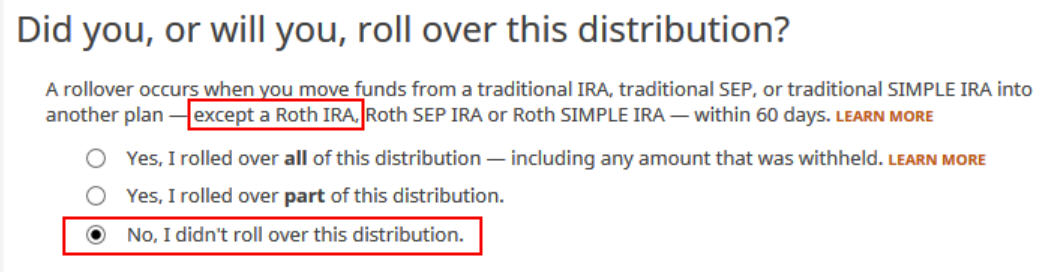

This can be a essential query. Learn rigorously. Reply No, since you transformed, not rolled over.

We don’t have these repaid withdrawals handled as rollovers.

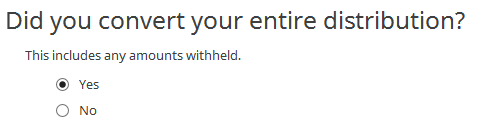

Now reply Sure, you transformed.

We transformed all of it in our instance.

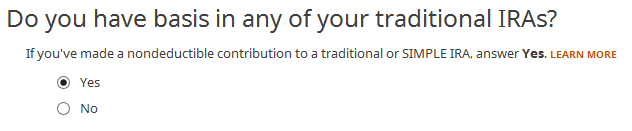

Reply Sure as a result of your contribution for the prior 12 months was your foundation.

The refund in progress drops quite a bit at this level. Don’t panic. It’s regular and solely short-term. It should come again up after we proceed.

You might be executed with this 1099-R. Repeat the above when you’ve got one other 1099-R. For those who’re married and each of you transformed to Roth, take note of whose 1099-R it’s once you enter the second. You’ll have issues in case you assign each 1099-Rs to the identical particular person once they belong to every partner. Click on on Completed if you find yourself executed with all of the 1099-Rs.

Extra Questions

H&R Block has a couple of extra questions.

Reply Sure in case you did a “clear” backdoor Roth in 2024 on high of changing your 2023 contribution, in different phrases, you additionally contributed to a Conventional IRA for 2024 in 2024 and transformed each your 2023 contribution and your 2024 contribution in 2024. Your 1099-R contains changing two 12 months’s value of contributions in a single 12 months.

For those who answered “Sure” to the earlier query, H&R Block will wait till you additionally enter your 2024 contribution. Your refund meter continues to be depressed however don’t fear.

For those who answered “No” to the earlier query since you didn’t contribute to a Conventional IRA for 2024, the software program will ask you to your foundation. Get that quantity from Line 14 of your Kind 8606. It’s $6,500 in our instance.

Clear Backdoor Roth On High

The conversion a part of the clear backdoor Roth is already included within the 1099-R type we simply accomplished. Now we do the contribution half.

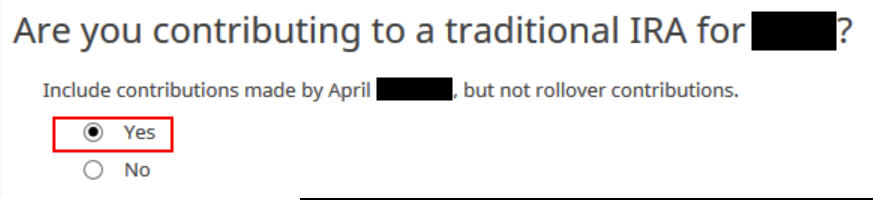

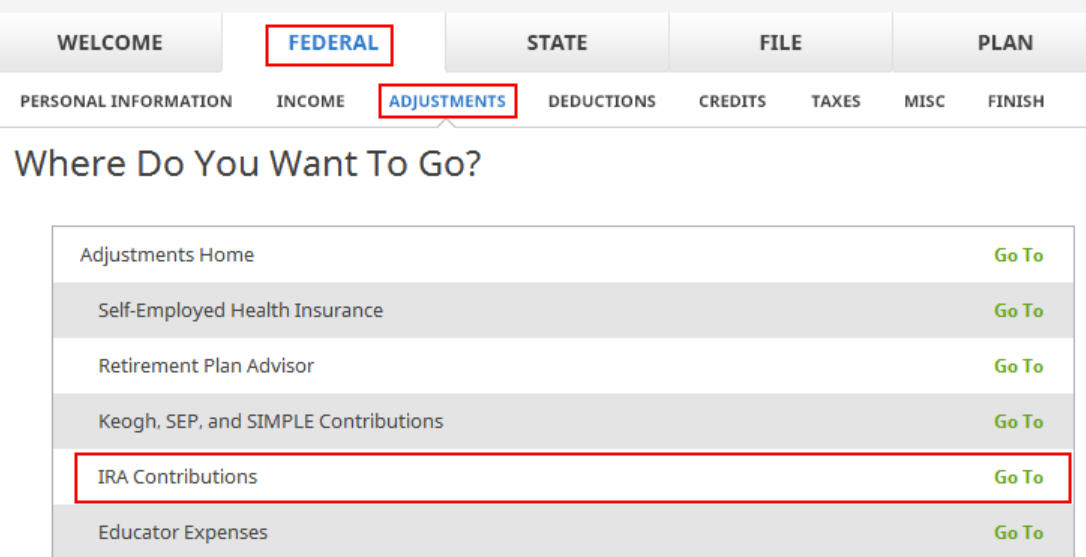

Click on on Federal -> Changes. Discover IRA Contributions. Click on on “Go To.”

Reply “Sure” since you contributed to a Conventional IRA in 2024 for 2024.

Examine the field for Conventional IRA.

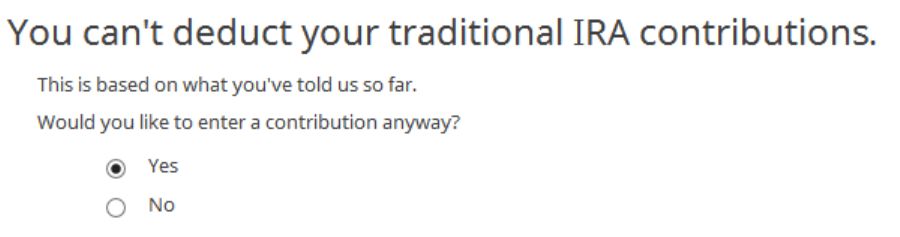

You recognize you don’t get a deduction attributable to revenue. Enter anyway. For those who don’t see this query, it means the software program thinks you’re eligible for a deduction. You possibly can’t decline the deduction.

Enter your contribution quantity. We contributed $7,000 in our instance.

Did Not Recharacterize

That is necessary. Reply No since you didn’t recharacterize. You transformed to Roth.

No extra contribution.

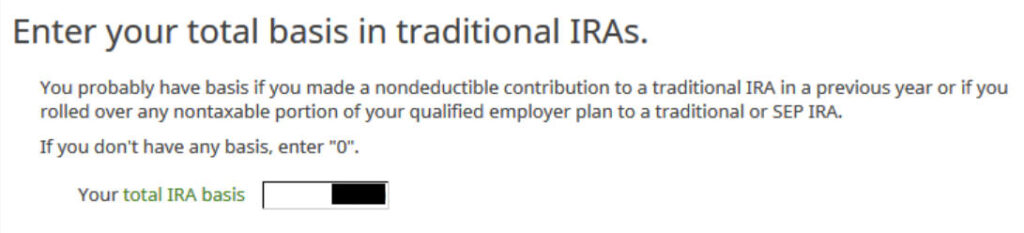

Foundation

H&R Block ought to import this from final 12 months’s knowledge nevertheless it doesn’t. Get it from final 12 months’s Kind 8606 Line 14. For those who didn’t have a Kind 8606 final 12 months as a result of the software program gave you a deduction on Schedule 1 Line 20, your foundation is zero. It’s $6,500 in our instance.

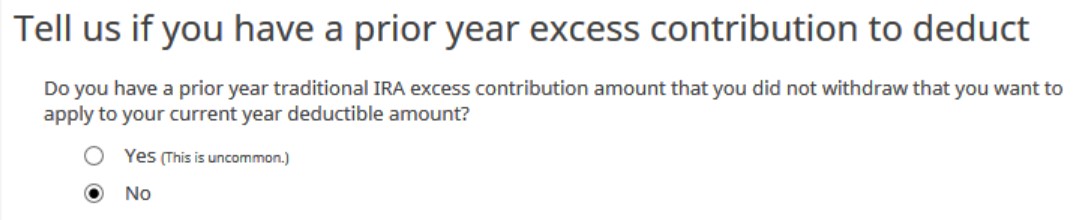

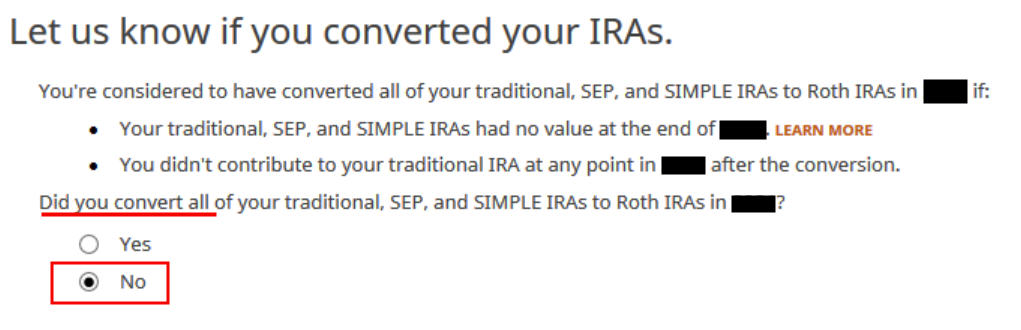

That is one other necessary query. For those who emptied all of your Conventional IRA and also you don’t have any SEP or SIMPLE IRAs, technically you’ll be able to reply Sure and skip some questions. The safer wager is to reply No and undergo the follow-up questions. For those who’ve been going by way of these screens backwards and forwards, you’ll have put in some incorrect solutions in a earlier spherical. You’ll have an opportunity to assessment and proper these solutions provided that you reply No.

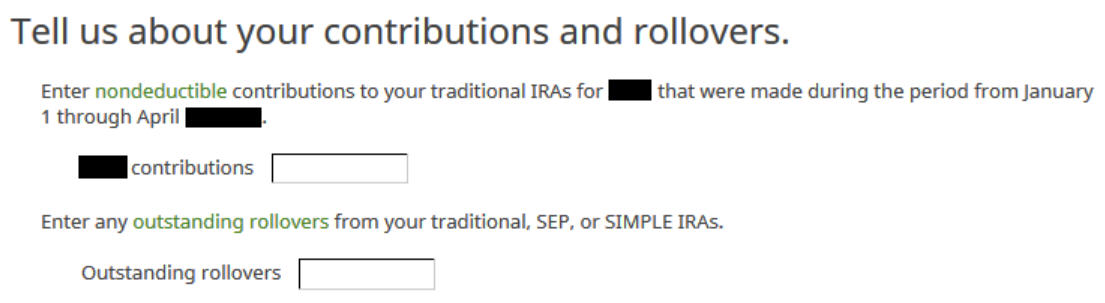

Go away the bins clean once you contributed for 2024 in 2024.

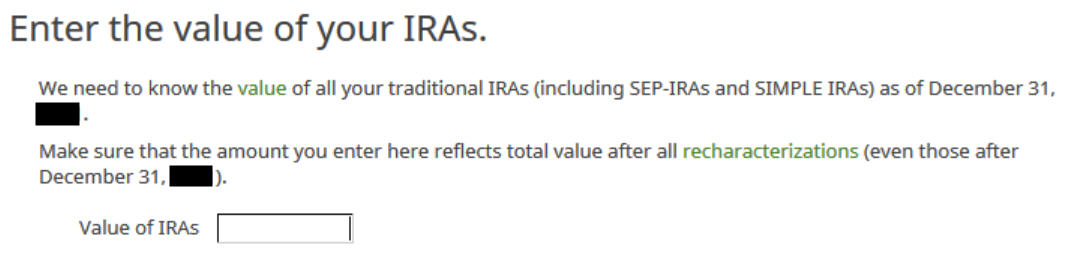

The field must be clean or zero once you emptied all of your Conventional IRAs after changing them to Roth. For those who had a couple of {dollars} of earnings after you transformed and also you left them within the account, get the worth out of your year-end statements and put it right here. The software program will apply the pro-rata rule.

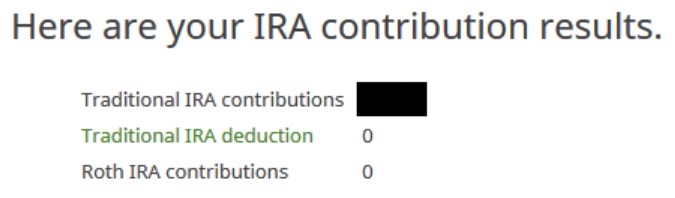

0 in Conventional IRA deduction means it’s nondeductible. Click on on Subsequent. Repeat to your partner if each of you contributed to a Conventional IRA.

Now the refund meter ought to return up after you enter the Conventional IRA contributions.

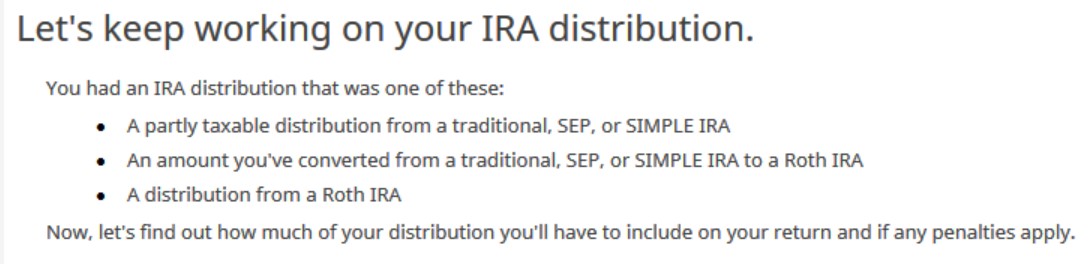

Taxable Earnings

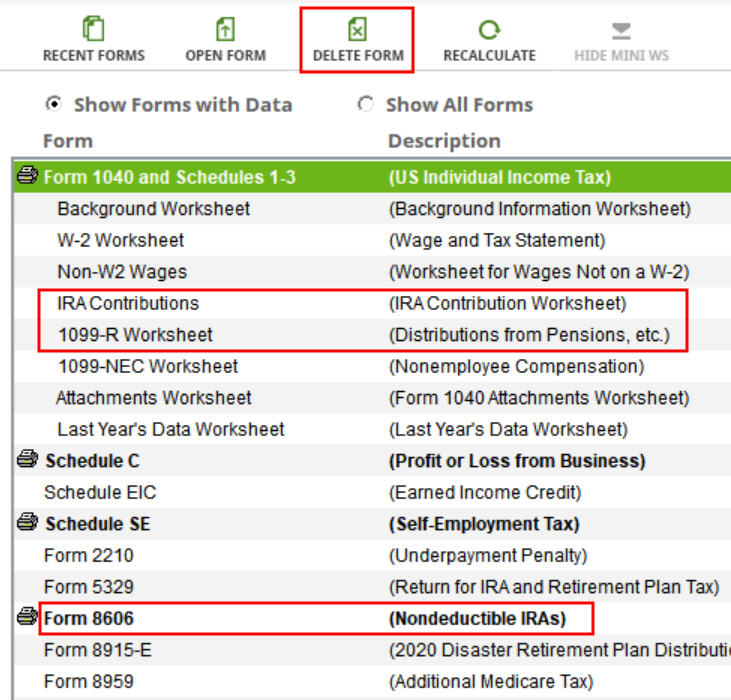

You’re executed with the 1099-R varieties. Let’s have a look at how they present up in your tax return. Click on on Kinds on the highest and open Kind 1040 and Schedules 1-3. Click on on Cover Mini WS. Scroll all the way down to traces 4a and 4b.

Line 4a exhibits the quantity in your 1099-R for the Roth conversion. Line 4b exhibits the taxable quantity, which is the earnings between the time you contributed to your Conventional IRA and the time you transformed it to Roth. The taxable quantity can be zero in case you didn’t have any earnings. The taxable quantity might be off by a couple of {dollars} attributable to rounding.

Kind 8606 exhibits these for our instance:

| Line # | Quantity |

|---|---|

| 1 | 7,000 (provided that you additionally did a “clear” backdoor Roth on high, in any other case clean.) |

| 2 | 6,500 |

| 3 | The sum of Line 1 and Line 2 |

| 5 | The identical as Line 3 |

| 13 | The identical as Line 3 (or near it attributable to rounding) |

| 14 | 0 |

| 16 | The quantity in your 1099-R with a code 2 or 7 |

| 17 | The identical as Line 3 (or near it attributable to rounding) |

| 18 | The distinction between Line 16 and Line 17 |

Troubleshooting

For those who adopted the steps and you aren’t getting the anticipated outcomes, right here are some things to examine.

Recent Begin

It’s greatest to comply with the steps contemporary in a single move. For those who already went backwards and forwards with totally different solutions earlier than you discovered this information, a few of your earlier solutions could also be caught someplace you now not see. You possibly can delete them and begin over.

Click on on Kinds and delete IRA Contributions Worksheet, 1099-R Worksheet, and Kind 8606. Then begin over by following the steps right here.

Conversion Is Taxed

For those who don’t have a retirement plan at work, you could have the next revenue restrict to take a deduction in your Conventional IRA contribution. When you have a retirement plan at work however your revenue is low sufficient, you might be additionally eligible for a deduction in your Conventional IRA contribution. The software program offers you the deduction if it sees that your revenue qualifies. It doesn’t provide the alternative of creating it non-deductible.

A part of your conversion might be taxed since you took a deduction on the Conventional IRA contribution final 12 months or this 12 months. You see whether or not you took a deduction by Schedule 1 Line 20 on final 12 months’s and this 12 months’s tax returns.

The taxable Roth IRA conversion and the deduction to your Conventional IRA contribution offset one another to create a wash. That is regular and it doesn’t trigger any issues once you certainly don’t have a retirement plan at work or when your revenue is sufficiently low.

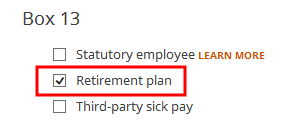

For those who even have a retirement plan at work, perhaps the software program didn’t see it. Whether or not you could have a retirement plan at work is marked by the “Retirement plan” field in Field 13 of your W-2.

Perhaps you forgot to examine it once you entered the W-2. Double-check the “Retirement plan” field in Field 13 of your (and your partner’s) W-2 entries to verify it matches the W-2.

Say No To Administration Charges

If you’re paying an advisor a share of your belongings, you might be paying 5-10x an excessive amount of. Discover ways to discover an impartial advisor, pay for recommendation, and solely the recommendation.

{kind=link}