Devon Power(NYSE: DVN) won’t be the best selection within the vitality patch for all buyers. That’s due to the kind of firm it’s, sitting solely within the upstream section of the trade. Nevertheless, extra aggressive buyers may really discover the corporate’s trade place enticing. Here is why some individuals will love Devon, and why others will probably need to keep away.

The large downside that numerous buyers can have with Devon is that it’s a pure play upstream vitality producer. Meaning its principal merchandise are oil and pure gasoline. These are extremely unstable commodities that undergo harrowing value swings. Every little thing from provide/demand dynamics to geopolitical occasions can result in giant and sometimes fast ups and downs.

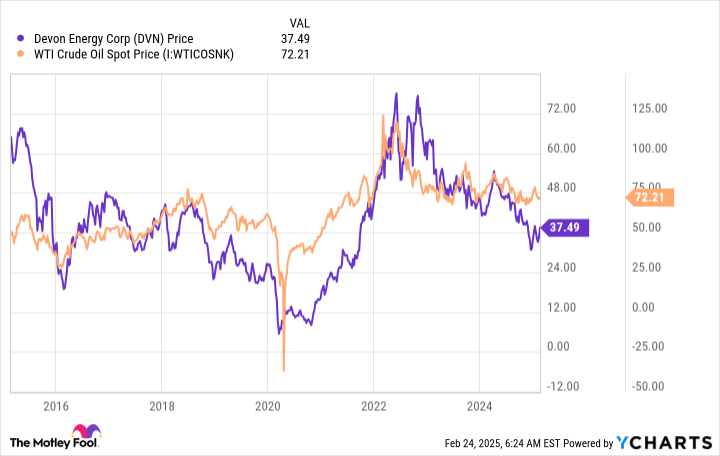

Rising vitality costs can have a optimistic impact on Devon’s income and earnings. Falling vitality costs can have the alternative impact. Since buyers are effectively conscious of those information, Devon’s inventory value will usually rise and fall together with the worth of West Texas Intermediate (WTI) crude, a key U.S. vitality benchmark.

On condition that dynamic, conservative buyers on the lookout for vitality publicity will in all probability be higher off trying elsewhere. place to begin can be corporations like Chevron(NYSE: CVX) or ExxonMobil(NYSE: XOM), that are each built-in vitality giants. They’ve extra diversified companies and, often, extra secure return profiles for buyers (notably, each have elevated their dividends for many years).

That mentioned, what should you’re seeking to put money into vitality in such a method as to leverage your self to rising vitality costs? That borders on market timing, which is a really troublesome factor to do effectively. However Devon Power can be a strong choice when you’ve got a constructive view of the vitality market.

There are a number of causes to love Devon Power on this rating. For starters, it has an funding grade-rated steadiness sheet, so it’s financially robust sufficient to climate adversity. It has operations in 5 main U.S. energy-producing areas, offering at the very least a modicum of diversification. Its manufacturing is break up pretty evenly between oil and pure gasoline, and the corporate has roughly a decade of land on which to proceed drilling.

Principally, Devon is a financially robust firm with a transparent path for continued success. In the event you consider vitality costs are probably to enhance, it is a pretty protected technique to again that perception with out taking a flyer on an organization that might find yourself in chapter courtroom in case your expectation for larger vitality costs falls flat.

Holding Devon Power is a little more nuanced. It does, clearly, seem to have the monetary power and enterprise basis to climate the ups and downs of the vitality sector. Notably, it has paid some stage of a dividend for a really very long time, because the chart beneath highlights. Whereas the dividend hasn’t been constant, the truth that one has been paid for thus lengthy speaks to Devon’s power as an organization. In that regard, you may justify it as a long-term method so as to add extra direct vitality publicity to your portfolio (maybe as a hedge to your real-world vitality prices).

There’s one other optimistic situation to contemplate right here. Devon Power has been performing as an trade consolidator, shopping for belongings which might be probably too small for vitality trade giants like Exxon and Chevron to take a look at. Nevertheless, given Devon’s comparatively small measurement, they’re notable additions to its portfolio. Meaning Devon is each a survivor and a rising enterprise on the identical time.

Sticking it out via the vitality cycle could possibly be a strong selection, assuming you perceive that vitality downturns will result in inventory value declines. The important thing is perhaps to view such downturns as alternatives so as to add extra to the inventory, should you prefer it sufficient to carry via the cycle.

Devon Power is by nature a unstable enterprise and a unstable inventory. Do not buy it if that’s going to hassle you. Nevertheless, in case you are on the lookout for a technique to put money into oil and pure gasoline, significantly within the U.S. market, it is a well-run firm with a strong historical past of surviving the trade’s inherent ups and downs. It’s most applicable for extra lively and extra aggressive buyers, after all, nevertheless it may simply fill the vitality area of interest of a portfolio fairly respectably — should you’re keen to just accept the inherently unstable nature of its enterprise.

Before you purchase inventory in Devon Power, think about this:

The Motley Idiot Inventory Advisor analyst group simply recognized what they consider are the 10 greatest shares for buyers to purchase now… and Devon Power wasn’t one among them. The ten shares that made the minimize may produce monster returns within the coming years.

Contemplate when Nvidia made this record on April 15, 2005… should you invested $1,000 on the time of our advice, you’d have $765,576!*

Now, it’s price notingInventory Advisor’s whole common return is890% — a market-crushing outperformance in comparison with173%for the S&P 500. Don’t miss out on the most recent high 10 record, obtainable once you be a part ofInventory Advisor.

*Inventory Advisor returns as of February 24, 2025

Reuben Gregg Brewer has no place in any of the shares talked about. The Motley Idiot has positions in and recommends Chevron. The Motley Idiot has a disclosure coverage.

{kind=link}