The brand new 2025 Trump tax legislation — One Massive Stunning Invoice Act — created a number of new tax deductions. Some folks thought they had been above-the-line deductions, however they’re all below-the-line. This publish explains the distinction between the various kinds of tax deductions.

Not a Tax Credit score

To begin with, a tax deduction just isn’t a tax credit score.

A tax credit score immediately reduces your tax dollar-for-dollar. If you happen to’re purported to pay $5,000 in tax, a $1,000 tax credit score reduces your tax to $4,000.

A tax deduction lowers your taxable revenue, which not directly reduces your tax. If you happen to’re purported to pay $5,000 in tax, a $1,000 tax deduction lowers your taxable revenue by $1,000, which then reduces your tax by a fraction of it, relying in your marginal tax fee.

Subsequently, a $1,000 tax deduction is price lots lower than a $1,000 tax credit score.

Inside tax deductions, there are above-the-line deductions, customary deduction, itemized deductions, and a set of deductions which can be neither above-the-line nor itemized.

Above-the-Line Deductions

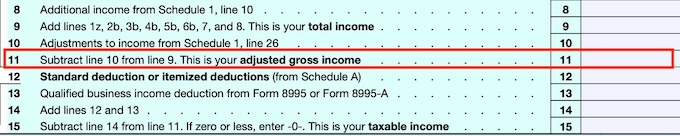

Above-the-line deductions are formally referred to as changes to revenue. The “line” refers back to the line on the tax kind on your Adjusted Gross Earnings (AGI). Your AGI is a key quantity that determines your eligibility for a lot of tax breaks. It’s the place to begin for Modified Adjusted Gross Earnings (MAGI) for varied functions, as an illustration, ACA medical insurance premiums and IRMAA.

A tax deduction is both above-the-line or below-the-line. Above-the-line deductions decrease your AGI and show you how to qualify for different tax breaks. Beneath-the-line deductions don’t have an effect on your AGI, they usually don’t show you how to qualify for different tax breaks.

Subsequently, a $1,000 above-the-line tax deduction is healthier than a $1,000 below-the-line deduction.

Solely particular tax deductions are designated as above-the-line. They’re listed on web page 2 of Type 1040 Schedule 1. Listed here are some examples:

- HSA contributions made outdoors of payroll

- Deductible Conventional IRA contributions

- Educator bills

- 1/2 of the self-employment tax

- Contributions to small enterprise retirement plans

- Self-employment medical insurance deduction

Normal Deduction Or Itemized Deductions

The usual deduction and itemized deductions come after the AGI. They’re below-the-line.

The usual deduction and itemized deductions are mutually unique. If you happen to select to take the usual deduction, you hand over itemizing your deductions. If you happen to select to itemize, you forego the usual deduction.

Usually, you itemize solely when the sum of your itemized deductions is larger than your customary deduction. You retain it easy and take the bigger customary deduction when you recognize you don’t have that a lot in itemized deductions.

Taking the usual deduction is a win since you’re deducting greater than your allowable itemized deductions. Over 80% of taxpayers take the usual deduction. So do I.

Itemized deductions are listed on Type 1040 Schedule A. Mortgage curiosity, state revenue tax, property tax, and donations to charities are typical itemized deductions (apart from the brand new $1,000/$2,000 charity donations deduction for non-itemizers).

Flooring and Caps

Simply because one thing is tax-deductible, it doesn’t imply you possibly can deduct 100% of it. It is because some deductions should first clear a ground.

For instance, medical bills are tax-deductible, however you possibly can solely deduct the portion that exceeds 7.5% of your AGI. That involves zero for many individuals.

Some deductions have a cap. You possibly can deduct solely as much as the cap, even if you happen to paid extra. State and native taxes (SALT) are a well known instance of this.

The brand new 2025 Trump tax legislation elevated the SALT cap. Extra individuals are anticipated to itemize deductions, however they’re nonetheless a minority. Over 80% of individuals will nonetheless take the usual deduction.

Beneath-the-Line, Accessible-to-All

Within the outdated days, individually recognized tax deductions had been both above-the-line or itemized deductions. Above-the-line deductions had been out there to each itemizers and non-itemizers. Beneath-the-line deductions had been solely the usual deduction or itemized deductions. After taking the above-the-line deductions, you might solely take the usual deduction if you happen to don’t itemize.

This dichotomy between above-the-line and must-itemize not holds. Congress has created a number of deductions lately which can be below-the-line however don’t require itemizing. You possibly can nonetheless take these deductions once you take the usual deduction, however they don’t have an effect on your AGI. A deduction out there to each itemizers and non-itemizers doesn’t essentially imply it’s above-the-line.

| Itemizers | Non-Itemizers | |

|---|---|---|

| Above-the-Line Deductions | ✅ | ✅ |

| Normal Deduction | 🚫 | ✅ |

| Itemized Deductions | ✅ | 🚫 |

| Beneath-the-Line, Accessible-to-All | ✅ (besides when particularly excluded) | ✅ |

Each above-the-line deductions and this new class of deductions can be found to everybody (besides when a deduction is particularly excluded). The distinction is in whether or not it impacts your AGI. Solely the usual deduction and itemized deductions are nonetheless either-or.

Congress created these below-the-line, available-to-all deductions as a result of they needed to make them extra extensively out there. Giving them to solely itemizers (10-20% of taxpayers) could be too limiting. However Congress didn’t need these deductions to decrease the AGI and set off different tax breaks. A few of these deductions themselves have limits based mostly on the AGI. Making them above-the-line would create a round math drawback.

Listed here are a few of the deductions that fall on this class of below-the-line available-to-all deductions:

All of those deductions are nonetheless out there if you happen to take the usual deduction, however they don’t decrease your AGI.

Say No To Administration Charges

In case you are paying an advisor a share of your property, you might be paying 5-10x an excessive amount of. Learn to discover an impartial advisor, pay for recommendation, and solely the recommendation.

{kind=link}